- Jun 16

- 8 min read

TECHTONICS

THE FUTURE FOR SALE

MINA CRANDON

June 16, 2026

Prediction markets present themselves as tools of reason, probability, and collective intelligence. Yet behind the charts and fluctuating odds lies a much older story. From prophets and mediums to economists and algorithms, every age has searched for a way to peer beyond the present. Mina Crandon examines the surprising continuity between ancient oracles and today’s online platforms where millions now bet on the future.

There was a time when people waited for the future to arrive. They read newspapers in the morning, watched election returns in the evening, and learned the outcome when the outcome became known. Today, many people experience events differently. Before a presidential election, a central bank decision, a ceasefire agreement, or even the winner of a television competition has occurred, thousands of individuals are already watching percentages fluctuate on prediction markets. One is trading at 58 percent. Then 61. Then 56. Millions of dollars change hands. Entire communities gather around probability charts that move in real time. The event itself increasingly feels like an afterthought. The real drama lies in the movement of the odds.

The rise of prediction markets represents one of the stranger developments of the twenty-first century. It is strange not because the technology is particularly revolutionary. The platforms themselves are relatively simple. Participants buy and sell contracts tied to future events. The price of those contracts is interpreted as the collective probability of an outcome occurring.

The mechanics are straightforward. The implications are not. For what prediction markets really offer is not merely a new form of betting, but a new way of imagining the future itself. In a culture increasingly uncomfortable with uncertainty, prediction markets transform tomorrow into something that can be quantified, traded, and monitored minute by minute. They represent the latest chapter in a much older story: humanity’s endless desire to know what comes next.

The desire is ancient. Long before spreadsheets, algorithms, and trading platforms, human beings sought signs. Ancient Mesopotamians examined the entrails of animals. Roman augurs studied the flight patterns of birds. Medieval rulers consulted astrologers before making military decisions. Kings and emperors surrounded themselves with prophets, seers, and advisors who claimed access to hidden knowledge. The methods varied. The impulse remained remarkably consistent.

Before probabilities, there were prophecies. The future was consulted rather than calculated.

Uncertainty has always been one of the fundamental problems of human existence. We know that events are coming. We do not know which events. We know that tomorrow exists. We do not know what it contains. This gap between the present and the future generates anxiety, and civilizations have repeatedly developed institutions designed to bridge it. One of the most famous examples is the Oracle of Delphi in ancient Greece. Visitors traveled considerable distances to consult a priestess believed to speak on behalf of the god Apollo. Generals sought military advice. Politicians sought guidance. Merchants sought reassurance. The answers were often cryptic enough to accommodate multiple interpretations, but that hardly mattered. The oracle provided something more valuable than certainty. It provided the feeling that uncertainty could be managed.

The modern world likes to imagine that it has left such practices behind. We tend to contrast ourselves with earlier societies, viewing ourselves as rational where they were superstitious, scientific where they were mystical. Yet the distinction is perhaps less clear than we imagine. The disappearance of the oracle did not eliminate the need for prediction. It merely created new oracles.

Today this ancient desire has found a new home on platforms such as Polymarket and Kalshi, where users buy and sell contracts tied to future events. Elections, interest-rate decisions, economic indicators, sporting events, celebrity scandals, and occasionally questions so obscure that one wonders who first thought to ask them all appear alongside one another. The premise is deceptively simple. If a contract predicting a particular outcome trades at sixty cents, the market is effectively assigning a 60 percent probability to that event occurring. The result is a constantly updating portrait of collective expectation, a numerical expression of what thousands of people believe the future is likely to contain.

One of humanity’s earliest forecasting technologies: uncertainty translated into signs.

Looking at these platforms, I was reminded less of Wall Street than of something much older. Human beings continue to search for institutions capable of transforming ignorance into knowledge, even when that knowledge turns out to be provisional, imperfect, and occasionally wrong.

Economists emerged. Pollsters emerged. Statistical models emerged. Television panels emerged. Entire industries developed around forecasting the future. Financial analysts predict stock movements. Political consultants predict elections. Demographers predict population changes. Think tanks predict international developments. Technology executives predict the next wave of innovation. The future became professionalized. The figures changed. The function remained.

One of the central intellectual assumptions behind modern prediction markets comes from the economist Friedrich Hayek. Hayek argued that knowledge is dispersed throughout society. No individual possesses all relevant information. Markets, however, can aggregate countless fragments of information through prices. A market price is not merely a number. It is a summary of many different judgments, expectations, and pieces of knowledge. This insight transformed economics. It also transformed forecasting.

Instead of asking experts what they think will happen, prediction markets ask a different question: What are people willing to risk money on? The assumption is that financial incentives encourage honesty. People may publicly support a candidate they secretly doubt. They may repeat fashionable opinions they do not truly believe. Money, however, introduces discipline. A trader who consistently ignores reality eventually loses capital. In theory, prediction markets convert beliefs into measurable commitments.

For centuries, rulers looked upward for answers. The stars functioned as a celestial market of expectations.

The result is a curious inversion. For centuries, societies looked upward for guidance. Truth descended from priests, kings, intellectuals, or institutions. Prediction markets reverse this: Truth emerges from below. No single participant possesses authority. Instead, authority is generated collectively through buying and selling. The market becomes a secular oracle.

This development reveals something important about contemporary culture. Modern societies often claim to distrust authority. Trust in governments has declined. Trust in traditional media has declined. Trust in experts has declined. Yet the need for authority has not disappeared. It has simply migrated.

Many people who would never place faith in a newspaper editorial or a government spokesperson will place remarkable faith in a fluctuating probability market. A chart displaying 63 percent somehow feels objective. The number appears neutral. Scientific. Beyond ideology. Whether this confidence is justified remains an open question.

Prediction markets have undoubtedly achieved impressive successes. They have often outperformed polling averages. They have correctly anticipated political outcomes dismissed by commentators. They have demonstrated a surprising ability to incorporate dispersed information quickly. Yet they are hardly infallible.

The economist who argued that markets aggregate knowledge no individual can possess alone.

Markets can panic. Markets can become euphoric. Markets can be manipulated. Markets are populated by human beings, and human beings remain vulnerable to emotion, herd behavior, wishful thinking, and collective delusion. The same mechanisms that allow markets to aggregate knowledge also allow them to aggregate mistakes. This tension is not a flaw in prediction markets. It is precisely what makes them interesting.

Prediction markets occupy an uncomfortable position between rationality and speculation. They are simultaneously serious forecasting tools and sophisticated gambling platforms. Advocates emphasize the former. Critics emphasize the latter. Both are correct. Indeed, one of the most fascinating aspects of prediction markets is the difficulty of distinguishing between information gathering and gambling. The distinction often appears clear in theory. It becomes considerably less clear in practice.

A person checks election odds every few minutes. He follows rumors on social media. He monitors trading volumes. He studies minute fluctuations in probability. He experiences excitement when the market moves in his favor and disappointment when it does not. Is he conducting research? Or is he gambling? The answer may be both.

Modern technology has a remarkable ability to transform ancient behaviors into respectable activities. Horse racing becomes data analysis. Sports betting becomes predictive modeling. Speculation becomes information gathering. The language changes more quickly than the underlying psychology. Prediction markets are particularly revealing because they emerge at the intersection of several larger trends. One is the financialization of everyday life.

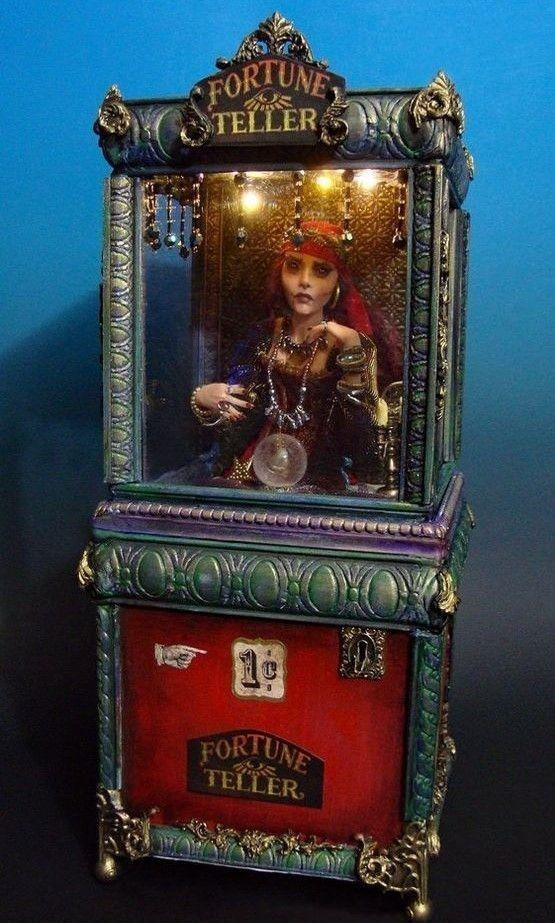

The oracle becomes mechanical, coin operated, and available to anyone with a penny.

Over the past century, markets have expanded into areas that previous generations would have considered unusual. Financial instruments have grown increasingly abstract. Derivatives are contracts based on other contracts. Futures markets trade events that have not yet occurred. Entire industries revolve around risk management and probability.

Prediction markets extend this logic further. Land can be traded. Labor can be traded. Debt can be traded. Attention can be traded. Data can be traded. Why not uncertainty itself?

From this perspective, prediction markets appear less like a radical innovation than the logical conclusion of a long historical process. Once societies become comfortable assigning monetary value to increasingly intangible things, assigning value to probabilities becomes almost inevitable. The future itself becomes a commodity.

Politics transformed into a continuously updating financial instrument.

This development would likely have seemed bizarre to earlier generations. Yet it feels strangely natural today. We inhabit a world saturated with measurement. Steps are counted. Sleep is tracked. Productivity is monitored. Social interactions are quantified through likes, followers, and engagement metrics. The transformation of uncertainty into numbers fits comfortably within this broader cultural landscape.

Everything is measurable. Everything is comparable. Everything is a score. Prediction markets extend this mentality into the future.

The result is a subtle shift in how events are experienced. Traditionally, uncertainty created suspense because outcomes remained unknown until they occurred. Prediction markets introduce a continuous stream of provisional knowledge. Before the event arrives, people already possess a detailed probability distribution describing possible outcomes. This changes the emotional texture of anticipation.

By the time an election occurs, many observers have spent months watching probabilities evolve. They have seen the future repeatedly simulated. They have watched confidence rise and fall. When the result finally arrives, it often feels less like a revelation than a settlement. Reality confirms the prevailing odds. The future arrives already priced in. This may help explain a peculiar feature of contemporary culture: the decline of surprise.

The modern temple of collective expectation, where information and speculation become indistinguishable.

Not because surprising events no longer happen. They do. Rather, because modern systems increasingly generate expectations in advance. Statistical models, polling aggregators, prediction markets, and algorithmic forecasts create a continuous pre-experience of future events. By the time reality arrives, people have often encountered dozens of hypothetical versions of it already. The event itself becomes strangely familiar. One suspects that this development has consequences beyond forecasting. It affects imagination. It affects politics. It affects culture. It may even affect our relationship to possibility. The future once represented a realm of mystery. Today it increasingly resembles a dashboard. Yet prediction markets reveal something even deeper than this. Their popularity exposes a profound discomfort with uncertainty itself.

Modern societies celebrate uncertainty rhetorically. Innovation requires uncertainty. Creativity requires uncertainty. Democracy requires uncertainty. Yet psychologically, uncertainty remains difficult to tolerate. We crave answers. We seek probabilities. We want numbers attached to possibilities.

Prediction markets satisfy this desire. They do not eliminate uncertainty. They merely give uncertainty a numerical form. A 58 percent probability still contains doubt. Yet doubt expressed as a percentage often feels more manageable than doubt expressed as ignorance. The number creates an illusion of control. Perhaps this is why prediction markets continue to attract attention even among people who never place a trade. Their deeper appeal is not financial. It is existential. They offer a framework for confronting the unknown.

The secular oracle speaks in percentages rather than riddles.

For centuries, people sought certainty from priests, prophets, philosophers, and experts. Today many seek it from charts and probabilities. The language has changed from revelation to forecasting, from destiny to percentages, from divine will to market sentiment. Yet the underlying impulse remains remarkably familiar. Prediction markets do not prove that humanity has become more rational. They suggest something more interesting. They suggest that every age invents institutions capable of transforming uncertainty into something that feels understandable. Ancient societies built temples. Modern societies build platforms. The desire is the same. The future remains unknowable. The mystery remains intact. The only difference is that we now watch it flicker across a screen, updating every few seconds, expressed to two decimal places, as if uncertainty itself had become just another thing for sale.

Ancient anxieties rendered as a user interface. The mystery remains; only the design has changed.

Mina Crandon (born in 1976 in Gloucester, Massachusetts) is a writer and essayist. She is best known for accurately predicting her admission to MIT at the age of fifteen and then refusing to attend. Since then, she has maintained a healthy suspicion of forecasts, experts, and people who claim to know what happens next. Her writing explores prophecy, probability, technology, finance, and other modern systems of belief. She lives in Athens.

Cover image: The future arrives years early, expressed as percentages and traded by strangers.

Comments